- Talking Shop with Gather Capital

- Posts

- What Keeps Me Up at Night About Continuation Funds?

What Keeps Me Up at Night About Continuation Funds?

What You Need to Be Watching Out For as an LP

Matthew Podlesak & Peter Kapp

July 11, 2024

Continuation funds can help both GPs & LPs, but there are also reasons LPs should be weary

Continuation funds are buzzing in the private equity (PE) world right now. Sure, they return money to LPs and fill a crucial gap, but there are key factors LPs need to keep an eye on.

As someone who diligences dozens of PE funds for high-net-worth clients at Gather Capital, I’ve watched the rise of continuation funds (CVs) closely. While market chatter highlights the benefits of CVs, it's critical for LPs to recognize potential conflicts that could impact their investments.

TLDR:

1. There are concerning conflicts between i) the GP, ii) existing fund LPs and iii) New CV LPs

2. GPs are likely to be biased towards creating CVs given economic benefits for the GP (potentially at expense of the LP)

3. Most of all… its the GP’s job to decide when to sell a company. That’s why we pay them 2&20. LPs should not have to take on this responsibility under sub-optimal conditions (lack of time / info / resources)

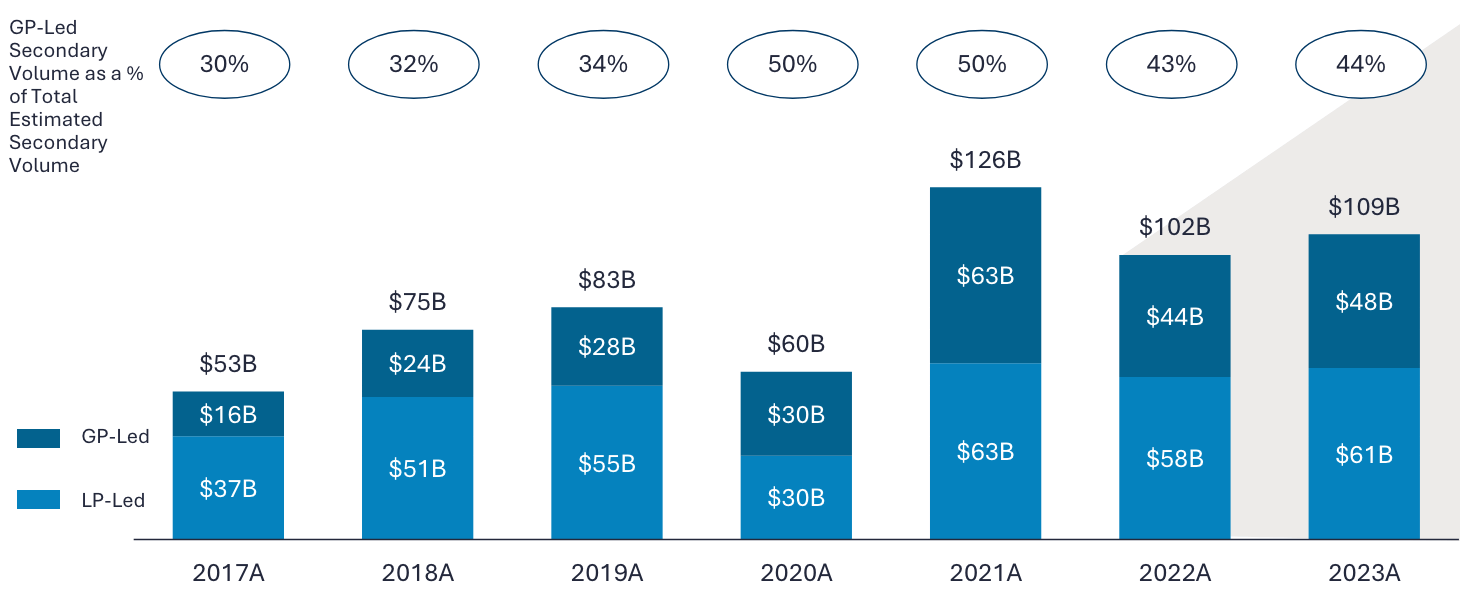

Source: Lazard

The Benefits of CVs

PE GPs tout several benefits of CVs:

Extended Value: LPs can ride the value wave of an asset beyond the fund’s life if the deal has untapped potential.

Early Liquidity: LPs can cash out sooner than with a traditional exit like a sale or IPO.

But these perks come with risks.

The Risks of CVs

The main issue? CVs create multiple classes of LPs with overlapping and conflicting interests. Here's what keeps me up at night about continuation funds:

1. Conflicted Interests Between GP & LP

For LPs cashing out of the PE fund but not rolling over into the CV:

The GP’s duty is to maximize the asset's sale price for the existing fund.

For new LPs entering the CV: The GP aims for the lowest possible price to boost the CV’s upside.

These conflicting loyalties can lead to two adverse outcomes:

GPs might maximize profits for legacy fund LPs cashing out.

GPs could prioritize new CV LPs at the expense of legacy fund LPs.

2. GP’s Adverse Incentives

Reasons why a GP might favor the CV over the fund:

Additional Carry: CVs offer GPs a chance for more carry beyond the fund's life, tempting them to create CVs to generate extra profits.

Extended Management Fees: GPs earn fees longer on the asset, often calculated off the asset’s value, increasing the fee base compared to the original committed capital.

LPs forced to decide whether to roll over or cash out face the risk of missing potential gains.

3. Challenges for LPs

Lack of Information: LPs often don’t get enough info to make an informed choice.

Limited Expertise: Many LPs lack the skills to navigate these complex deals, especially smaller investment teams without secondary transaction experts.

Tight Deadlines: With just 10–20 days to decide, LPs are under intense pressure, making well-informed decisions tough.

No Status Quo Option: Rolling over can feel coercive when the only choices are contributing new capital or accepting new terms, especially if the continuation fund is established early.

Diversification Issues: Single-asset funds can disrupt portfolio balance and increase risk, while some LPs cash out to maintain liquidity or rebalance their investments.

Continuation funds fill a gap, but LPs need to be vigilant about these hidden risks. Understanding these dynamics helps navigate the complexities of PE investing more effectively.

At Gather Capital, we strive to curate a set of world class alternative investment opportunities, especially within private equity, that enable our clients to invest alongside many of these elite family office limited partners.

We are investing into a wide range of opportunities from:

multi-billion dollar sized funds from blue-chip firms with multi-decade track records of top tier returns…

…to sub-billion dollar sized funds led by highly sought after emerging managers.

If you’re interested in learning more about what we do, feel free to:

swing by our website & create an account (if you haven’t already)

grab some time on our calendar here

shoot us an email

We’re looking forward to Talking Shop with you soon.

Sincerely,

Ben Chideckel Co-Founder | Gather Capital 211 E. 43rd Street, Suite 900 New York, NY 10017 |  Matthew G. Podlesak Co-Founder | Gather Capital 211 E. 43rd Street, Suite 900 New York, NY 10017 |